Not long after my spouse and I began spending time together, he mentioned that he had student loans.

“How much?” I asked.

He paused. “About $150,000.”

As one of the first people in his family to go to college, Amos* was caught in a situation common to turn of the century Americans. College, he repeatedly heard, was how you avoid minimum-wage jobs—but neither his family nor his school advised him on how to select a good degree program. His parents made too much for need-based aid but not enough to pay for his degree, and he lost a scholarship when he failed one class.

Amos racked up private loans, then refinanced when he couldn’t afford the payments. This lowered his monthly payments… by extending his loans to thirty years, with more interest for the lender.

When we met, he was about thirty, making less than $3000 USD a month, and paying half of that each month in debt, mostly interest. He was scheduled to finish paying for college when he retired.

It wasn’t the most promising situation.

But we took a chance, and not long after we eloped, we snuggled up in a hotel room to… fill out spreadsheets and analyze which debt to tackle first (Never say I’m not a romantic…).

~~~

So it was particularly heartwarming recently to watch Amos sit a younger friend down and guide him through the steps to pay off his own loan. As I eavesdropped, I smiled to hear Amos talk Chris* through much of what we’d done ourselves.

1. Choose which debts to pay first.

Gather your statements and write down how much you owe on each debt, the interest rate, and your monthly payment.

We used this Excel calculator to see the impact of paying more each month, or changing which loan we paid first. It helps you visualize the difference between paying the loan with the highest interest rate first (a “debt avalanche”), or paying the smallest loans first (a “debt snowball”), so you feel like you’re moving ahead. Both have benefits.

We updated this chart every few months, and it was encouraging to see our end date move up from the year 2044 to 2019 (!!) as we made bonus payments over time.

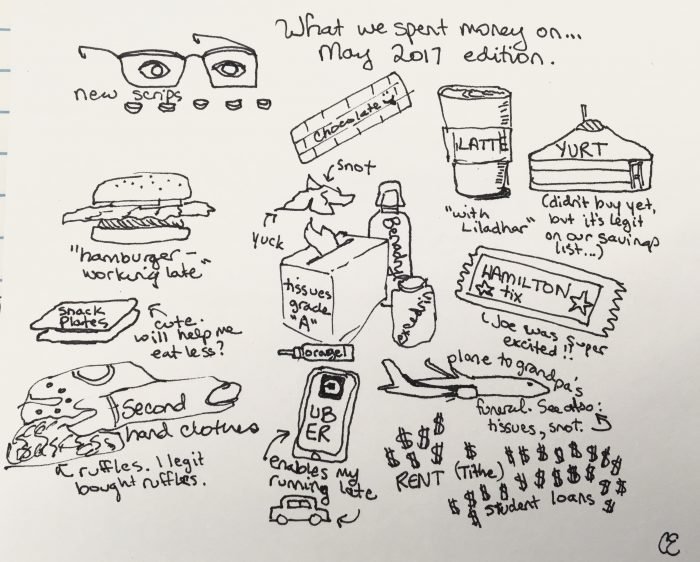

2. Track where your money goes.

As I’ve written before, we’re not planners. So we started gently, just setting up automatic tracking to see where our money goes. As Amos says,

“It gives you a better idea of where your money is actually going. You spend money on your card and it’s easy to get to the end of a month and say, I don’t feel like I spent that much. But you can look back and see—well, I ate out three times and bought these five things at a convenience store…”

I found this helpful so that, even when we focused intensely on paying down debt, we could see that we did still spent on stuff we enjoyed. For example,

3. Plan where your money will go next month.

Next, we needed to plan. As Amos told Chris,

“Then, figure out what you can spare or save. For me it was things like cutting back on subscriptions to audiobooks or on hobbies—maybe you do half as much. Not cut back entirely, because it will just make you miserable, but just enough to make a difference.”

Amos was never a fan of sell-your-car-and-eat-rice extreme frugality. He still wanted to do sports like fencing and archery and eat out with friends. So he planned for that—and I planned for reading, coffee, and travel—my preferences!, by trying out different planning apps like EveryDollar, YNAB, and Mint.

4. Create an emergency fund.

Amos also suggested that Chris try to save $200 out of his $4000/month salary into an emergency fund. (I would have said pay off all your loans tomorrow! . . . but this is why I’m not the one giving advice).

Chris decided he could maybe cancel his streaming subscriptions and use library media, or pack a lunch for work for a few months. Some people have trouble cutting things, but he had a healthy enough income to work with. And if he could save up $1000 or so, it would help him avoid using credit if his car breaks down or he has an unexpected medical expense.

5. Pay the first debt… and then the next one.

With an emergency fund to protect him from banks making money off his life emergencies, Amos then suggested that Chris put bonuses, and overtime pay into the debt he’d chosen to pay first:

“Put any money you can save as an extra payment on your highest interest loan. And keep rolling it. Whenever you get a bonus or tax return, take a bit for fun, then put the rest toward the debt.”

And so on. Once the first loan is closed, celebrate, then tackle the next one.

This is what we did to pay off $130,000 on Amos’ loans, which ended up costing about $141,000 with interest, plus opportunity costs; we closed them down within three years of marriage.

~~~

While writing this up, I asked Amos for other tips he’d share with others trying to pay down loans, based on his experience. His thoughts:

Find social support

For a long while, Amos was ashamed and didn’t talk about finances, not even telling his family when he was struggling. But coming out in the open and finding supportive people can make the process easier.

In his case, Amos jokingly noted the importance of a financially stable partner, saying,

“Marry someone who doesn’t have debt, and doesn’t like spending money. That was definitely a help!”

Yes, he’s fortunate to have married me 😀 and more seriously, we’re fortunate to have been able to find good salaries and pay down loans quickly. I’m not sure I could have signed a marriage contract if I’d also had high loans, as it might have pulled us both under.

And even then it was hard. I I depended heavily on friends and family for emotional support as I struggled with the weight of a debt and constraints I wasn’t used to.

Wherever you’re at, finding people who are supportive can really help.

Keep a progress chart

As Amos notes,

“Keeping a record of what you started with is helpful. It’s super easy to end up in the middle and say, I still have so much left to go. I feel like I’m not making any impact. We had that a couple of times. And we could look back and say, yeah, we paid off $60,000 already.”

We recognized the progress we’d made, and celebrated each time we ticked off another $10,000 or so.

Look for new work opportunities

Ironically, the fact that I moved to California right as we started dating helped us. When he first moved to join me, he couldn’t find a job with a salary as good as he’d had back home—but then he moved companies and got a raise, and another one. While moving to a city isn’t an option for everyone, for Amos, “switching jobs and locations definitely helped.”

In the end, moving into a growing economy helped us to pay off loans faster, even with the higher rent and taxes here.

Be flexible with housing

When Amos graduated from college, he was eager to live on his own, yet he graduated into the 2008 global economic crisis, making it hard to find work that paid enough to make rent, save an emergency fund, and make progress on his loans.

His younger brother has been more fortunate, landing a great job in a bull market and and living with family for free while he pays off loans. If you have such a chance, use it.

As a couple, we lived with housemates in our first year together, which lowered our rent by $1000 a month. This let us quickly pay down principal on our debt and bought us time until we could both get raises, helping us afford to live on our own in an expensive city.

Avoid loans if possible

Obviously, as Amos now reflects, “The best option is not to get the debt to begin with.”

Ideally, student loans would finance a degree that offers a significant financial and social benefit over not going to college, and could be fully paid off with less than 10% of your income in the first ten years after college. Otherwise, it may not be worth going into that program at all.

For example, I had the opportunity to study for a master’s in writing in Australia, but turned it down because it required loans. Through patience, I later got two master’s degrees (anthropology, libraries) fully funded without debt on my part. Saying no to the wrong college financing was very helpful in being able to say yes to the right degree later.

If you’re considering degrees, I hope you’ll find a similar opportunity.

And if you’re one of the many people still working on student loans, I wish you the best in paying them down quickly.